|

Gold closed at 634.20 dollars an ounce on Friday, up 0.4% from $631.60 at the close of the previous Friday. The dollar closed at 0.7791 euros Friday, down 0.6% from 0.7841 for the week. That put the euro at 1.2836 dollars compared to 1.2753 at the end of the previous week. Gold in euros, then, would be 494.08 euros an ounce, down 0.3% 495.37 for the week. Oil closed at 69.19 dollars a barrel Friday, down 4.8% from $72.51 at the end of the previous week. Oil in euros would be 53.90 euros a barrel, down 5.5% from 56.86 for the week. The gold/oil ratio closed at 9.17, up 5.3% from 8.71 at the end of the week before. In the U.S. stock market, the Dow closed at 11,464.15, up 1.6% from 11,284.05 at the close of the previous week. The NASDAQ closed at 2,193.16, up 2.5% from 2140.29 for the week. In U.S. interest rates, the yield on the ten-year U.S. Treasury note closed at 4.72% Friday, down five basis points from 4.79 for the week.

The monthly jobs report was released last week and the estimated job growth was 128,000, which cheered the analysts and the stock market. It was just large enough to convince people that the economy is not collapsing but small enough to keep inflation fears at bay. Lots of talk about "easing" growth and such:

Data Point To Cooler Growth, Steady Rates

By Tim Ahmann

Fri Sep 1, 4:18 PM ET

U.S. employers added 128,000 workers to their payrolls in August, evidence of a cooler -- but still solid -- pace of economic growth that could let the Federal Reserve hold interest rates steady.

The closely watched Labor Department report, issued on Friday just ahead of the Labor Day holiday weekend, showed the unemployment rate dipped to 4.7 percent from 4.8 percent in July, suggesting the job market remains sturdy.

Other reports on Friday showed a slight slowing in factory activity last month and big drops in both construction spending and pending home sales in July that offered the latest evidence of the faltering U.S. housing market.

But consumer sentiment held up better in August than many economists had expected and analysts said the economy appeared to be decelerating, though not abruptly.

"It looks an awful lot like a soft landing, at least for now," said Dana Johnson, chief economist at Comerica Bank in Detroit. "It's an economy that is not firing on all cylinders -- it's got a clear concentration of weakness in the housing sector -- but, otherwise, an economy that is moving ahead at something resembling a trend-like pace."

The deluge of data left financial markets comfortable with bets that the U.S. central bank has finished raising interest rates and would turn to cut them next year, with bond prices and the dollar little changed.

Stock prices, however, got a boost, as investors welcomed the not-too-hot, not-too-cold economic picture. The blue chip Dow Jones industrial average closed up 83 points.

INFLATION TEA LEAVES

The closely watched employment report showed a slight pickup in payroll growth after an upwardly revised 121,000 job gain in July and was largely in line with analysts' forecasts.

Some details, however, were softer than expected.

Average hourly earnings rose a slim 2 cents, or 0.1 percent, last month. While that left the 12-month gain at a five-year high of 3.9 percent, economists had braced for a sharper monthly rise.

In addition, the length of the average work week dipped by 0.1 hour to 33.8 hours, pulling down an index of overall hours worked, in a potential sign of softer growth.

"All in all, it's a very inflation-friendly and Fed-friendly report," said Richard Yamarone, chief economist at Argus Research in New York. "It doesn't suggest any economic frailty, but it supports a sidelined Fed."

After raising benchmark borrowing costs in 17 small steps dating back to June 2004, the Fed stepped to the sidelines at its last meeting on August 8 and held interest rates steady.

Interest-rate futures contracts put the implied chances of a increase in borrowing costs at the Fed's next meeting on September 20 at only about 6 percent after Friday's data.

A Reuters poll of 21 top Wall Street firms that deal directly with the Fed in the markets found only one expecting a rate rise later this month. Twelve said the Fed was likely finished raising rates.

FACTORIES COOLER, HOUSING ON ICE

Separately, the Institute for Supply Management said its index of factory activity slipped to 54.5 in August from 54.7 in July, showing continued growth at a slightly slower pace.

At the same time, the prices paid index fell to 73.0 from 78.5, a sign of receding price pressures.

Another report showed consumer sentiment falling in August, but by less than expected. The University of Michigan's sentiment index fell to 82.0 from 84.7 in July.

Two other reports combined to underscore the sharp weakening that has been evident in the U.S. housing market.

The Commerce Department said construction spending tumbled by 1.2 percent in July, the biggest drop since August 2001, as spending on homebuilding plummeted 2 percent.

At the same, the National Association of Realtors said its index of pending homes sales -- a gauge of contracted sales waiting to close -- plunged 7 percent in July to the lowest level in more than three years. The drop was the biggest on records dating to 2001.

The jobs report, however, showed construction payrolls expanded by 17,000 in August, with residential construction employment up marginally for a second straight month.

Today is Labor Day in the United States. The U.S. celebrates Labor Day in September rather than May 1, when the rest of the world does, because Communists and Socialists celebrate May 1, and we can't have any of that. The veterans group in the town I live in put up American flags on all the telephone poles. What nationalism has to do with Labor Day, I can't imagine, but some people can't imagine a holiday without nationalism or religion. But I have to say, fascist sentiment has almost completely drained away from the general public in the United States. Much of this is due to the clear and complete disaster of the Iraq war. Some of it also has to do with the public pessimism about the economy as housing values are falling, wages are stagnant, and job and pension security are practically non-existent, while the few at the top make out like bandits. The propaganda meisters will have their work cut out for them in convincing the public to attack Iran. If we survive Bush's presidency, maybe that will prove to be his achievement: completely discrediting fascist nationalism, fundamentalist Christianity and Republican economic policy by his extreme incompetence. A person can hope, anyway.

As for U.S. labor, Jason Miller points out that upper class gains have come right out of the pocket of workers, and that most people realize this:

Labor's Pains

Friday, September 01, 2006

In 1898, Samuel Gompers, one of the original founders of the American Federation of Labor, called Labor Day "the day for which the toilers in past centuries looked forward, when their rights and their wrongs would be discussed." This Labor Day, U.S. workers have many grievances that deserve attention. The New York Times reported recently that the median real hourly wage for American workers has declined two percent since 2003, despite the fact that productivity has been steadily rising. Worker productivity rose 16.6 percent from 2000 to 2005, while total compensation for the median worker rose 7.2 percent. Among the reasons economists offer to explain this phenomenon are that workers' bargaining power is being slowly eroded and "trade unions are much weaker than they once were." The trends have left U.S. workers feeling bleak about the future. A poll of laborers conducted recently found that 63 percent of the workforce believes the country and the economy are on the wrong track; a majority now believe their children are going to be worse off economically than they are. The Progress Report details some of the problems facing today's workforce:

WORKING HARDER, EARNING LESS: "Wages and salaries now make up the lowest share of the nation's gross domestic product since the government began recording the data in 1947." A majority of today's workers say the number one issue they face is that the wages they are paid are not keeping up with the cost of living. Aug. 20th marked 10 years since the last time the federal minimum wage has been raised. Frozen at an unlivable $5.15/hour, the minimum wage is at the lowest buying power it has been in 51 years. Workers earning above the minimum wage are struggling as well. According to AFL-CIO President John Sweeney, "Real median earnings for men working full-time and year-round were lower in 2005 than in 1973. In inflation-adjusted 2005 dollars, a typical man working full-time in 1973 earned $42,573. Thirty-six years later, this figure has fallen to $41,386." Yet, productivity -- as President Bush likes to frequently point out -- remains high. "What jumps out at you is the gaping hole between productivity growth and earnings," said Jared Bernstein, an economist at the Economic Policy Institute (EPI). People are "working harder and smarter but not really seeing remuneration that they ought to be seeing." The wage crunch isn't affecting the entire labor force, however. The top one percent of earners -- including many corporate CEOs -- received 11.2 percent of all wage income in 2004, up from 8.7 percent a decade earlier and less than six percent three decades ago.

SICK ABOUT HEALTH CARE: According to new Census data released this week, the number of people living in the United States without medical insurance rose 2.9 percent -- 1.3 million people -- to a record 46.6 million over the last year alone as health-care costs climbed three times as fast as wages. The statistics indicate 6.8 million people have lost coverage since 2001, and this total has climbed every year since Bush has been in office. The Census Bureau also reports the percentage of uninsured children rose from 10.8 percent in 2004 to 11.2 percent in 2005 due to state budget struggles. This reverses a trend that started in 1998 of declining uninsured rates for children. "Due to the rising cost of health care and health-care insurance, you see a continued decline in workers accepting coverage when it's offered and employers offering it," said Emory University Professor Ken Thorpe. Indeed, three million people have lost employer-based insurance, while the rate of uninsured, full-time workers has increased by 13 percent since 2000. The bottom line is sadly simple: "Uninsured workers can't afford to get sick." Ultimately, this is a moral question -- it is wrong for anyone who works hard and plays by the rules to go without health coverage. "People who don't have coverage, can't afford preventive care, and don't see a doctor until a disease has progressed often suffer needlessly, drive up the cost of care, and lower the nation's productivity."

ORGANIZED VOICES BEING REPRESSED: In a recent report on the boom in profits, economists at Goldman Sachs wrote plainly, "The most important contributor to higher profit margins over the past five years has been a decline in labor's share of national income." "If I had to sum it up," said Bernstein, "it comes down to bargaining power and the lack of ability of many in the work force to claim their fair share of growth." Wal-Mart, America's largest employer and heralded as the corporate model for today's economy, has opposed every effort of its employees to form a union. (Ironically, Wal-Mart has given its approval to its China-based workers organize.) "According to Cornell labor relations professor Kate Bronfenbrenner, at least 5 percent of workers involved in unionization campaigns are fired, which is both quite illegal and quite routine: Companies would rather pay the nominal fines than pay their workers higher wages and lose the absolute control they hold over the work lives of their employees." Today's labor movement faces union-busting law firms and consulting agencies which are increasingly enlisted by union-wary employers to keep labor from organizing. Today, the vast majority of union members -- 84 percent -- live in only 12 states, leaving workers with little organized power in much of the country. But despite internal struggles in the past, union leaders are now making moves to unite and mobilize workers around "pocketbook" issues.

While wages were up slightly (but not in inflation-adjusted terms) last week saw the release of some frightening personal saving data:

Personal saving -- DPI less personal outlays -- was a negative $83.5 billion in July, compared with a negative $67.6 billion in June. Personal saving as a percentage of disposable personal income was a negative 0.9 percent in July, compared with a negative 0.7 percent in June. Negative personal saving reflects personal outlays that exceed disposable personal income. Saving from current income may be near zero or negative when outlays are financed by borrowing (including borrowing financed through credit cards or home equity loans), by selling investments or other assets, or by using savings from previous periods.

Negative saving rates are a trend that simply cannot continue forever. As The Roxylander in Flame blogger puts it:

The Hole In The Pants Gets Bigger

The consumer spending rose by 0.8% in July and personal savings are -0.9%, which means the average consumer is spending 0.9% more than his salary is.

As noted here, the 16-months period of negative savings is the longest since the Great Depression.

Do you like the news that a certain economic indicator is the worst since the Great Depression? So do I, my friends, so do I.

On the housing bubble front, the following piece by Mike Whitney was published on the Signs page last week but bears reposting:

Pop Goes the Bubble!

The Great Housing Crash of '07

By Mike Whitney

August 30, 2006

This month's figures prove that the so-called "housing bubble" is not only real, but that its cratering faster than anyone had realized. As the UK Guardian reported just yesterday, "the orderly housing slowdown predicted by the Federal Reserve will (soon) become a full-blown crash".

All the indicators are now pointing in the wrong direction. Consumer confidence is down, inventory is at a 10 year high, and the number of homes sold in July was 22% lower than last year. As Paul Ashworth, chief economist at Capital Economics said, "Things seem to be getting worse very quickly. Freefall is a strong word, but I think it's the right one to use here." (UK Guardian)

The housing bubble is a $10 trillion equity balloon that will explode sometime in 2007 when more than $1 trillion in no-interest, no down payment, adjustable-rate mortgages (ARMs) reset; setting the stage for massive home devaluation, foreclosures and unemployment. ("By some estimates housing activity has accounted for 40% of all the jobs created since 2001". Times Online) July's plunging sales are just the first sign of a major slowdown. The worst is yet to come.

The blame for this rapidly-approaching meltdown lies entirely with the Federal Reserve, the privately-owned collection of 10 central banks who cooked up a way to shift wealth from one class to another through low interest rates.

Sound crazy?

Well, just as high interest rates cause the economy to slow down; low interest rates have the exact opposite effect by stimulating the economy through increased spending. It's all pretty clear-cut.

When the stock market nose-dived in 2000 the Fed lowered rates 17 times to an unbelievable 1% to keep the economy sputtering-along while the Bush administration dragged the country to war, gave away $450 billion a year in tax cuts, and awarded zillions in no bid contracts to their friends in big business. All tolled, the Bush-handouts amounted to roughly $3 trillion dollars, the largest heist in history, and it was carried out under the nose of the snoozing American public.

At the same time, America's debts and deficits have continued to mushroom behind the smokescreen of low interest rates.

Rather than face the recession which should have followed stock market crash, the Fed chose to increase the money supply (which doubled in the last 7 years) and lower the qualifications for getting mortgages. (I read recently that 90% of first time home buyers not only lie on their mortgage applications, but that 50% of them say that they earn TWICE as much as they really do. The applications are not cross-checked with IRS statements) Now, tens of thousands of Americans live in $400,000 and $500,000 homes without a penny of equity in them and with loans that are timed to increase dramatically in 2007. (Many of the monthly payments will double)

So, how can we blame the Fed for the reckless and irresponsible behavior of the average homeowner?

Well, because they knew the effects of their "cheap money" policy every step of the way.

First of all, the Fed knew exactly where the money was going. Greenspan endorsed the shabby new lending-regime which put hundreds of billions of dollars in the hands of people who never should have qualified for mortgages. They were set up to fail just like the victims in the stock market scam who kept dumping their life savings in the NASDAQ when PE's were shooting through the stratosphere.

Secondly, the Fed knew that wages had actually regressed (2.3%) since Bush took office, so they knew that the soaring value of real estate was entirely predicated on debt not real wealth. In other words, home values increased because of the availability of cheap money which inevitably creates a buying-frenzy. It had nothing to do with real demand or growth in wages.

And, thirdly, according to the Fed's own figures, "the total amount of residential housing wealth in the US just about doubled between 1999 and 2006, up from $10.4 trillion to $20.4 trillion". Times Online.

UP $10 TRILLION IN 7 YEARS! That is the very definition of a humongous, economy-killing equity monster. In other words, the Fed knew the ACTUAL SIZE OF THE BUBBLE and chose to steer it towards the nearest iceberg without warning the public.

This is what Greenspan called "a little froth".

There is no real growth in the American economy. Figure it out. Last year Americans saved less than 0% of their net earnings while they borrowed a whopping $600 billion from their home equity to piss-away on a consumer spending-spree. Once home prices begin to retreat, that $600 billion will evaporate, real GDP will shrivel, and the economy will begin flat-lining. (Consumer spending is 70% of GDP)

The Federal Reserve's plan is so simple; we shouldn't dignify it by calling it a conspiracy. It's merely a matter of hypnotizing the masses with low interest rates while trillions of dollars of real wealth is diverted to corporate big-wigs and American plutocrats.

It might not be rocket science, but it worked like a charm.

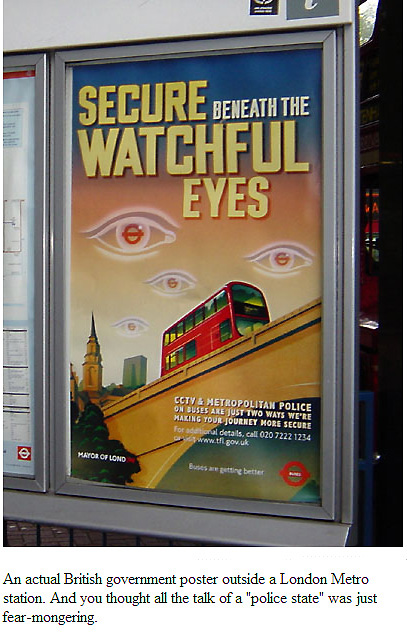

Now, the trap-door has been sprung; the country is dead-broke and all the levers are in place for a police state. As the housing-balloon slowly limps towards earth, the new Halliburton detention centers are up and running, the National Guard is in Rummy's control, the Feds are able to listen-in on every phone call we make.

The noose is beginning to tighten.

New Orleans was just a dress rehearsal for the new world order; 300,000 million Americans reduced to grinding poverty while the economy explodes into sheets of flames.

Now that it is too late, publications such as Business Week are sounding the alarm about risky mortgages:

Nightmare Mortgages

They promise the American Dream: A home of your own -- with ultra-low rates and payments anyone can afford. Now, the trap has sprung

For cash-strapped homeowners, it was a pitch they couldn't refuse: Refinance your mortgage at a bargain rate and cut your payments in half. New home buyers, stretching to afford something in a super-heated market, didn't even need to produce documentation, much less a downpayment.

Those who took the bait are in for a nasty surprise. While many Americans have started to worry about falling home prices, borrowers who jumped into so-called option ARM loans have another, more urgent problem: payments that are about to skyrocket.

The option adjustable rate mortgage (ARM) might be the riskiest and most complicated home loan product ever created. With its temptingly low minimum payments, the option ARM brought a whole new group of buyers into the housing market, extending the boom longer than it could have otherwise lasted, especially in the hottest markets. Suddenly, almost anyone could afford a home -- or so they thought. The option ARM's low payments are only temporary. And the less a borrower chooses to pay now, the more is tacked onto the balance.

The bill is coming due. Many of the option ARMs taken out in 2004 and 2005 are resetting at much higher payment schedules -- often to the astonishment of people who thought the low installments were fixed for at least five years. And because home prices have leveled off, borrowers can't count on rising equity to bail them out. What's more, steep penalties prevent them from refinancing. The most diligent home buyers asked enough questions to know that option ARMs can be fraught with risk. But others, caught up in real estate mania, ignored or failed to appreciate the risk.

There was plenty more going on behind the scenes they didn't know about, either: that their broker was paid more to sell option ARMs than other mortgages; that their lender is allowed to claim the full monthly payment as revenue on its books even when borrowers choose to pay much less; that the loan's interest rates and up-front fees might not have been set by their bank but rather by a hedge fund; and that they'll soon be confronted with the choice of coughing up higher payments or coughing up their home. The option ARM is "like the neutron bomb," says George McCarthy, a housing economist at New York's Ford Foundation. "It's going to kill all the people but leave the houses standing."

Because banks don't have to report how many option ARMs they underwrite, few choose to do so. But the best available estimates show that option ARMs have soared in popularity. They accounted for as little as 0.5% of all mortgages written in 2003, but that shot up to at least 12.3% through the first five months of this year, according to FirstAmerican LoanPerformance, an industry tracker. And while they made up at least 40% of mortgages in Salinas, Calif., and 26% in Naples, Fla., they're not just found in overheated coastal markets: Through Mar. 31 of this year, at least 51% of mortgages in West Virginia and 26% in Wyoming were option ARMs. Stock and bond analysts estimate that as many as 1.3 million borrowers took out as much as $389 billion in option ARMs in 2004 and 2005. And it's not letting up. Despite the housing slump, option ARMs totaling $77.2 billion were written in the second quarter of this year, according to investment bank Keefe, Bruyette & Woods Inc.

The First Wave

After prolonging the boom, these exotic mortgages could worsen the bust. They also betray such a lack of due diligence on the part of lenders and borrowers that it raises questions of what other problems may be lurking. And most of the pain will be borne by ordinary people, not the lenders, brokers, or financiers who created the problem.

Gordon Burger is among the first wave of option ARM casualties. The 42-year-old police officer from a suburb of Sacramento, Calif., is stuck in a new mortgage that's making him poorer by the month. Burger, a solid earner with clean credit, has bought and sold several houses in the past. In February he got a flyer from a broker advertising an interest rate of 2.2%. It was an unbeatable opportunity, he thought. If he refinanced the mortgage on his $500,000 home into an option ARM, he could save $14,000 in interest payments over three years. Burger quickly pulled the trigger, switching out of his 5.1% fixed-rate loan. "The payment schedule looked like what we talked about, so I just started signing away," says Burger. He didn't read the fine print.

After two months Burger noticed that the minimum payment of $1,697 was actually adding $1,000 to his balance every month. "I'm not making any ground on this house; it's a loss every month," he says. He says he was told by his lender, Minneapolis-based Homecoming Financial, a unit of Residential Capital, the nation's fifth-largest mortgage shop, that he'd have to pay more than $10,000 in prepayment penalties to refinance out of the loan. If he's unhappy, he should take it up with his broker, the bank said. "They know they're selling crap, and they're doing it in a way that's very deceiving," he says. "Unfortunately, I got sucked into it." In a written statement, Residential said it couldn't comment on Burger's loan but that "each mortgage is designed to meet the specific financial needs of a consumer."

The loans certainly meet the needs of banks. Option ARMs offer several payment choices each month. Among Burger's alternatives were one for $2,524, about what a standard fixed-rate mortgage would be on the new amount, and the $1,697 he pays. Why would his bank make the minimum so low? Thanks to a perfectly legal accounting practice, no matter how little Burger pays each month, the bank gets to record the full amount.

Option ARMs were created in 1981 and for years were marketed to well-heeled home buyers who wanted the option of making low payments most months and then paying off a big chunk all at once. For them, option ARMs offered flexibility.

So how did these unusual loans get into the hands of so many ordinary folks? The sequence of events was orderly and even rational, at least within a flawed system. In the early years of the housing boom, falling interest rates made safe fixed-rate loans attractive to borrowers. As home prices soared, banks pushed adjustable-rate loans with lower initial payments. When those got too pricey, banks hawked loans that required only interest payments for the first few years. And then they flogged option ARMs -- not as financial-planning tools for the wealthy but as affordability tools for the masses. Banks tapped an army of unregulated mortgage brokers to do what needed to be done to keep the money flowing, even if it meant putting dangerous loans in the hands of people who couldn't handle or didn't understand the risk. And Wall Street greased the skids by taking on much of the new risk banks were creating.

Now the signs of excess are crystal clear. Up to 80% of all option ARM borrowers make only the minimum payment each month, according to Fitch Ratings. The rest of the money gets added to the balance of the mortgage, a situation known as negative amortization. And once balances grow to a certain amount, the loans automatically reset at far higher payments. Most of these borrowers aren't paying down their loans; they're underpaying them up.

Yet the banking system has insulated itself reasonably well from the thousands of personal catastrophes to come. For one thing, banks can sell some of their option ARMs off to Wall Street, where they're packaged with other, better loans and re-sold in chunks to investors. Some $182 billion of the option ARMs written in 2004 and 2005 and an additional $83 billion this year have been sold, repackaged, rated by debt-rating agencies, and marketed to investors as mortgage-backed securities, says Bear, Stearns & Co. (BSC) Banks also sell an unknown amount of them directly to hedge funds and other big investors with appetites for risk.

The rest of the option ARMs remain on lenders' books, where for now they're generating huge phantom profits for some lenders. That's because, according to generally accepted accounting principles, or GAAP, banks can count as revenue the highest amount of an option ARM payment -- the so-called fully amortized amount -- even when borrowers make only the minimum payment. In other words, banks can claim future revenue now, inflating earnings per share.

For many industries, so-called accrual accounting, which lets companies book sales when they contract for them rather than when they receive the cash, makes sense. The revenues will eventually come. But accrual accounting doesn't apply well to option ARMs, since it's more difficult to know if unpaid interest will ever cross a banker's desk. "This is basically an IOU that may never get paid," says Robert Lacoursiere, an analyst at Banc of America Securities. James Grant of Grant's Interest Rate Observer recently wrote that negative-amortization accounting is "frankly a fraudulent gambit. But what it lacks in morality, it compensates for in ingenuity." The Financial Accounting Standards Board, which is responsible for keeping GAAP up to date, stands by its standard but told BusinessWeek in a written statement that it is "concerned that the disclosures associated with these types of loans [are] not providing enough transparency relative to their associated risks."

Camouflaged Losses

Risks or not, the accounting treatment is boosting reported profits sharply. At Santa Monica (Calif.)-based FirstFed Financial Corp. (FED), "deferred interest" -- what an outsider might call phantom income -- made up 67% of second-quarter pretax profits. FirstFed did not respond to requests for comment. At Oakland (Calif.)-based Golden West Financial Corp. (GDW), which has been selling option ARMs for two decades, deferred interest made up about 59.6% of the bank's earnings in the first half of 2006. "It's not the loan that's the problem," says Herbert M. Sandler, CEO of World Savings Bank, parent of Golden West. "The problem is with the quality of the underwriting."

In the middle of one of the hottest U.S. markets, Coral Gables (Fla.)-based BankUnited Financial Corp. (BKUNA) posted a $14.8 million loss for the quarter ended June, 2005. Yet it reported record profits of $23.8 million for the quarter ended in June of this year -- $20.9 million of which was earned in deferred interest. Some 92% of its new loans were option ARMs. Humberto L. Lopez, chief financial officer, insists the bank underwrites carefully. "The option ARMs have gotten a bit of a raised eyebrow because we generate and book noncash earnings. But...it's our money, and we do feel comfortable we'll get it back."

Even the loans that blow up can be hidden with fancy bookkeeping. David Hendler of New York-based CreditSights, a bond research shop, predicts that banks in coming quarters will increasingly move weak loans into so-called held-for-sale accounts. There the loans will sit, sequestered from the rest of the portfolio, until they're sold to collection agencies or to investors. In the latter case, a transaction on an ailing loan registers on the books as a trading loss, gets mixed up with other trading activities and -- presto! -- it vanishes from shareholders' sight. "There are a lot of ways to camouflage the actual experience," says Hendler.

There's no way to camouflage what Harold, a former computer technician who asked BusinessWeek not to publish his last name, is about to face. He's disabled and has one source of income: the $1,600 per month he receives in Social Security disability payments. In September, 2005, Harold refinanced out of a fixed-rate mortgage and into an option ARM for his $150,000 home in Chicago. The minimum monthly payment for the first year is $899, which he can afford. The interest-only payment is $1,329, which he can't. The fully amortized payment is $1,454, which his lender, Washington Mutual (WM), gets to count on its books. WaMu, no fly-by-night operation, said it couldn't comment on Harold's case, citing confidentiality issues. A spokesman says the bank "accounts for its option ARM product in accordance with generally accepted accounting principles." WaMu has about $12 billion in loans negatively amortizing right now, up from $2.5 billion in 2005, estimates CreditSights' Hendler. In a written statement, WaMu said "borrowers who request an adjustable loan with payment options should understand those options and potential adjustments throughout the life of the loan. We make detailed disclosures to customers that are designed to develop a more informed consumer of mortgage products and ensure that our customers are comfortable with the loan products they select."

Hard Sell

To get the deals done, banks have turned increasingly to unregulated mortgage brokers, who now account for 80% of all mortgage originations, double what it was 10 years ago, according to the National Association of Mortgage Brokers. In 2004 banks began offering fatter sales commissions on option ARMs to encourage brokers to push them, says Gail McKenzie, assistant U.S. attorney in Atlanta, who is investigating mortgage brokers for improper practices.

The problem, of course, is that many brokers care more about commissions than customers. They use aggressive sales tactics, harping on the minimum payment on an option ARM and neglecting to mention the future implications. Some even imply verbally that temporary teaser rates of 1% to 2% are permanent, even though the fine print says otherwise. It's easy to confuse borrowers with option ARM numbers. A recent Federal Reserve study showed that one in four homeowners is mystified by basic adjustable-rate loans. Add multiple payment options into the mix, and the mortgage game can be utterly baffling.

Billy and Carolyn Shaw are among the growing ranks of borrowers who have taken out loans they say they didn't understand. The retired couple from the Salinas (Calif.) area needed to tap about $50,000 in equity from their $385,000 home to cover mounting expenses. Billy, 66, a retired mechanic, has diabetes. Carolyn, 61, has been caring for her grandchildren, 10-year-old twins, since her daughter's death in 2000. The Shaws have a fixed income of $3,000 a month that will fall by about $1,000 in November after Billy's disability benefits run out. Their new loan's minimum payment of about $1,413 is manageable so far, but the fully amortized amount of about $3,329 is out of the question. In a little over a year, they've added some $8,500 to their loan balance and now face a big reset if they continue to pay only the minimum. "We didn't totally understand what was taking place," says Carolyn. "You have to pay attention. We didn't, and we're really stuck here." The Shaws' lender, Golden West, says it routinely calls customers to ask them if they are happy and understand their mortgage loan.

Then there's the illegal stuff. Mortgage fraud is one of the fastest-growing white-collar crimes in the nation, costing $1 billion in 2005, double the year before. A slower housing market could foster more wrongdoing. "With a tighter market, you are going to find there is more incentive to manipulate," says Tim Irvin of Irvin Investigations & Research Services in Spring, Texas. "Brokers are having a harder time getting business, so they're getting creative..."

The practices of the mortgage industry, and indeed the whole financial system, expose a system much worse than merely "flawed" as the Business Week reporter put it. It should be clear to anyone with a working conscience that the neoliberal economic system, like most others, has been set up by and for psychopaths. The fact that the article details case after case of morally repugnant behavior by the lenders BEFORE getting to the "Then there's the illegal stuff." That means of course that a whole array of conscienceless lending practices are legal. We have to ask ourselves, what kind of people wrote these laws?

What do the banks say when challenged?

Analyst Frederick Cannon of Keefe Bruyette & Woods says most banks don't apologize for their option ARM businesses. "Almost without exception everyone says [the option ARM] is a great loan, it's plenty regulated, and don't bug us," he says. In an April letter to regulators, Cindy Manzettie, chief credit officer for Fifth Third Bank in Cincinnati, said it's not the "lender's responsibility to help the consumer determine the appropriate payment option each month.... Paternalistic regulations that underestimate the intelligence of the American public do not work."

I suppose Ms. Manzettie thinks that banks that precisely estimate the intelligence of the American public and devise products to that public do "work." As usual, the psychopath is skilled at using words with a twisted meaning. Surely these practices work in a selfish sense for those using them. But they don't work for society as a whole, and it is time for those in the Anglo-American world to question the big lie of neoliberalism: that that which benefits a few psychopaths at the top benefits us all.

|

![[Valid Atom 1.0]](/signs/images/valid-atom.png "Validate my Atom 1.0 feed")