|

Gold closed at 555.20 dollars an ounce on Friday, up 0.2% from 554.20 for the week. The dollar closed at 0.8375 euros Friday, down 0.3% from 0.8401 at the end of the previous week. That puts the euro at 1.1940 dollars, compared to 1.1904 the Friday before. Gold in euros would be 464.99 euros an ounce, down 0.1% from 465.56 the week before. Oil closed at 59.88 dollars a barrel, down 3.3% from $61.84 for the week. Oil in euros would be 50.15 euros a barrel, down 3.6% from 51.95 the week before. The gold/oil ratio closed at 9.27 up 3.5% from 8.96 at the end of the previous week. In the U.S. stock market, the Dow closed at 11,115.32, up 1.8% from 10,919.05 the Friday before. The NASDAQ closed at 2,282.36, up 0.9% from 2,261.88 the week before. The yield on the ten-year U.S. Treasury note closed at 4.54 down four basis points from 4.58 last Friday. There was much optimism about the U.S. economy from mainstream analysts last week, buoyed by rising stocks and falling oil prices (down 3.3%) and, for a while, falling gold prices (gold actually ended up a bit). The hope is that fresh quarterly earnings reports from major retailers this week will keep the U.S. stock market rising: Stocks could see 3rd week of gains By Caroline Valetkevitch Stock bulls will push for a third week of gains after last week's slide in oil to below $60 a barrel, but investors will be on the alert for signs of inflation and higher interest rates.

The Presidents' Day holiday-shortened week will include a rush of earnings from retailers, including Wal-Mart Stores Inc., which will grab investors' attention. After this coming Tuesday's closing bell, China's leading Web search company, Baidu.com, also will report quarterly results. The reports will put the finishing touches on the fourth-quarter corporate profit picture, which analysts said has improved since January when some high-profile companies disappointed Wall Street. Minutes on Tuesday from the Federal Reserve's January policy-setting meeting and consumer price data on Wednesday will be picked apart for further clues about the interest-rate outlook. Investors are worried signs of rising inflation will force the Fed to keep extending its long campaign of raising interest rates. The Fed has been tightening credit since June 2004 in an attempt to rein in inflation. New Fed Chairman Ben Bernanke, in congressional testimony last week, suggested that more rate increases may be needed to contain inflation. But analysts said his reassuring comments on the economy and the absence of any big surprises in his remarks helped push stocks higher. "His testimony not only played well to Congress, but to Wall Street. So we should continue to get a little honeymoon spillover from that," said Fred Dickson, senior vice president and market strategist at D.A. Davidson & Co. in Montana. In another positive sign for higher stock prices, crude oil last week fell below $60 for the first time this year. U.S. crude for March delivery was still below that level on Friday; it settled at $59.88 a barrel, up $1.42 on the New York Mercantile Exchange.

"Investors are going to go into the week feeling a little bit better about the shape of consumer spending and feeling much better about the emergence of Bernanke as he heads the Fed," Dickson said. By Friday's closing bell, all three major U.S. stock indexes had finished the week with gains. The blue-chip Dow Jones industrial average rose 1.8 percent, while the broad S&P 500 advanced 1.6 percent, and the Nasdaq Composite Index gained 0.9 percent. Oil's Drop Below $60 Forecasts of higher U.S. crude and gasoline inventories triggered the fall in oil to below $60 a barrel last Tuesday. On Wednesday, when a larger-than-expected rise in crude stockpiles was reported by the government, oil fell below $58 for the first time since late December. Lower energy prices tend to boost stocks because they mean reduced costs for consumers and corporations. But analysts said continued tensions between the Western powers and Iran over Iran's nuclear ambitions, as well as fighting in Nigeria, the eighth-largest crude exporter, between government forces and militants, could keep oil prices higher.

On Saturday, three American oil workers were abducted in Nigeria and the United States has called for their unconditional release. Militants stormed an offshore barge operated by U.S. oil services company Willbros Group Inc. in predawn attacks and abducted nine workers in all. Crude hit an all-time high of $70.85 in late August after Hurricane Katrina struck the U.S. Gulf Coast. "We don't think $60 is sustainable. We just had the warmest January in 100 years, but we're expecting colder temperatures in New York this weekend. Investors are being very short-sighted," said Philip Orlando, senior portfolio manager at Federated Investors. "We're sitting on a geopolitical powder keg with Iran that could blow at any moment. It would not surprise us to see crude back in the $70-plus neighborhood by the end of the quarter." Fed Minutes, Cpi And Durable Goods The financial markets will be closed on Monday for the Presidents Day holiday. But Wall Street will reopen on Tuesday anxiously awaiting the release of minutes from the Federal Open Market Committee meeting on January 31 -- Alan Greenspan's last. In the week ahead, the FOMC news will be followed on Wednesday by the consumer price index and on Friday by durable goods orders. Both reports, for January's data, will shed more light on the U.S. economy's health. "The market is hypersensitive to any clues that they can get as to what the Fed will do over the course of the tightening cycle," Orlando said. On Friday, a report from the Labor Department showing the core Producer Price Index, excluding volatile food and energy prices, climbed 0.4 percent in January -- twice market expectations -- was a negative influence for stocks. Economists polled by Reuters expect the overall CPI for January to rise 0.5 percent, after December's decline of 0.1 percent. They see core CPI, excluding volatile food and energy prices, up 0.2 percent in January, following December's gain of just 0.1 percent. Orders for durable goods, which are manufactured goods like washing machines, computers and cars designed to last three years or more, are expected to drop 1.0 percent in January, according to the Reuters poll. In December, durable goods orders rose 1.8 percent. Excluding transportation, January durable goods orders are forecast to rise 0.5 percent, compared with December's gain of 1.7 percent. From Wal-Mart To Nordstrom

Earnings will be on the watch list, too. In the week ahead, investors will get more insight into consumer spending when earnings come in from retailers ranging from discounters to purveyors of luxury goods.

Quarterly earnings are due on Tuesday from Wal-Mart, the discount behemoth and the world's largest retailer, as well as from Federated Department Stores Inc., the parent of Macy's and Bloomingdale's, and Home Depot Inc., the world's largest home improvement retailer. On Thursday, quarterly results are expected from Gap Inc., the largest specialty apparel chain; Nordstrom Inc., an upscale department store chain known for service and designer clothes; Kohl's Corp., a moderately priced department store chain, and Limited Brands Inc., owner of Victoria's Secret and Bath & Bodyworks stores. They follow higher profits reported last week by J.C. Penney Co. Inc. and Target Corp., which were boosted by strong holiday season sales. The fourth quarter generates the biggest portion of retailers' annual profit. "Good news on retailers should be a sigh of relief," Dickson said Yet, this optimism is coming at a time of record triple deficits, the hollowing out of productive capacity and the end of the asset bubble. And by productive capacity, I don't mean only industrial production. The offshoring of jobs has spread to core white collar jobs as well. The Pace of White-Collar Outsourcing

How rapidly will outsourcing of U.S. white collar jobs proceed? The consensus bet is 300,000 a year, but it all depends on how rapidly the English-literate populations of emerging markets expand: India's Outsourcing Industry Is Facing a Labor Shortage - New York Times By SARITHA RAI MUMBAI, India, Feb. 16 India's leadership in global outsourcing may be in jeopardy unless it increases its supply of skilled workers.... Experts... said Thursday that an incipient skills shortage was the biggest threat to the industry's blazing growth.... Pramod Bhasin, chief executive of Genpact, a back-office outsourcing company once owned by General Electric, set the tone when he said, If the talent in India is scarce, we will go wherever the labor pool is available. Lower-cost centers like Eastern Europe and China could become serious rivals for outsourcing business from Western multinational companies. Until now, corporations mainly looked to India to do work from customer support to writing software code to designing chips. But the supply of India's famed skilled, low-cost, English-speaking work force may not quite match the sizzling demand. India's $23.4 billion outsourcing industry accounts for most of the country's software and services industry, which makes up nearly 5 percent of gross domestic product. The industry employs 1.2 million workers, has sparked a consumer revolution in India, and is accelerating at more than 30 percent a year. On the sidelines of the Nasscom meeting, B. Ramalinga Raju, chairman of India's fourth- largest outsourcing company, Satyam Computer Services, said that India produced three million college graduates every year, including nearly 400,000 engineers. But most of these are uncut diamonds that have to go through polishing factories, as the trade requires only polished stones, Mr. Raju said. In a country of 1.1 billion people, raw talent is plentiful, he said, but not all of it is market-ready.... The supply shortfall is even more acute in mid-level jobs, like software engineers. Salaries in this segment are rising an average 20 percent a year, and in some segments even 50 percent annually, compared with 5 percent annual raises for software engineers in the United States. The irony is that while the outsourcing industry partially fueled an economic boom amongst the middle classes, the growth has now spilled onto other areas offering ambitious young college graduates an array of job options outside of the outsourcing industry, said M. S. Krishnan , professor of business information technology at the Stephen M. Ross School of Business at the University of Michigan.... Outsourcing companies are taking matters into their own hands to meet mid-level skills shortages by setting up vast, dedicated training centers. Tata Consultancy Services... has a large training center in Trivandrum... its nearest rival, Infosys Technologies, has a training campus in Mysore.... At any given point in time, there are 4,000 people in the pipeline at Infosys's training center, Mr. Krishnan said. Many companies believe the skills deficit will only grow. We are in the people business, and the situation will become more challenging in five years, said Amitabh Ray, director of global delivery, IBM Global Services India.... The situation is much the same in the back-office and call center jobs: of 100 college graduates applying, only 8 are immediately employable. Another 20 require considerable training to be hired, according to Nasscom data... The fact that the demand for Indian engineers is so strong that even a country as populous as India cannot keep up with it says a lot for the rapid pace of the gutting of higher-paid western office and professional workers. The type of shift that used to take a generation, enough time to be trained, to work for a career then retire, now takes place in less than a decade. Even India is fearing that their boom will end and their new jobs will go to lower-paid workers in China. One reason this is important is that standard economics says that if the dollar falls in value, the trade deficit can be turned around. Yet that presupposes productive capacity in the United States that can produce goods for export. But if that capacity has been completely gutted, then there can be no rebalancing. The following is from Stephen Roach, Chief Economist of Morgan Stanley: Global: Trade Deficits and Asset Bubbles

Stephen Roach (New York)

Most believe that the dollar holds the key to global rebalancing. Academics are especially adamant on this point, with many maintaining that it will take at least a 20-30% drop in the greenback to fix the US external imbalance. Yet that remedy doesn't square with the raison d'être of America's trade deficit. The problem is concentrated on the import side of the equation, driven largely by the excesses of asset-dependent consumption. That means higher real interest rates are likely to be far more important than a weaker dollar in resolving America's external imbalances. The latest US trade report says it all. In December 2005, imports of foreign goods and services ($177.2 billion) were fully 59% larger than exports ($111.5 billion). Moreover, it turns out that a -$70.6 billion deficit on goods was cushioned by a $4.9 billion surplus on services. Within the goods component of the December trade gap, the disparity between imports ($149.6 billion) and exports ($79.0 billion) was even larger. This underscores the daunting arithmetic of a turnaround to America's external imbalance. With goods imports fully 89% larger than goods exports, even if exports grow at twice the rate of imports, the deficit on goods will remain essentially unchanged. In other words, just from an arithmetic point of view, it will be exceedingly difficult for the United States to export its way out of its trade deficit. The export solution also suffers from an even more glaring deficiency -- the hollowing of Smokestack America. With manufacturing capacity and jobs moving steadily offshore over the past 20-plus years, the US simply lacks the wherewithal to spark an export-led turnaround in foreign trade. In all too many cases, the loss of US manufacturing prowess has been a permanent, or structural, erosion. The list of lost industries -- from steel and autos to textiles and even computers -- speaks of a competitive dynamic that makes it all but impossible for the US to recapture its once leading market share as an industrial powerhouse. As I noted recently, that leaves the US on the outside looking in when one of its formerly large trading partners like Japan springs back to life (see my 10 February dispatch, Rebalancing Made in Japan?). I am certain there is a level of the dollar that might reverse this process. But I think it is well in excess of the 20-30% decline that many believe is the answer to America's massive trade imbalance. Given the structural tilt to the global playing field, my guess is that in order to make a meaningful difference to America's trade dynamics on both the export and import sides of the equation, the US currency would have to be sustained at an exchange rate on the order of 30-50% below present levels on a broad trade-weighted basis. And the key word here is sustained. A trading blip will not give US exporters the confidence -- or the economics -- they need to go back into business. Needless to say, the odds are quite low that either the US or other global authorities would accept such a dollar-collapse scenario as a palliative for America's trade deficit . Largely for those reasons, I think it is safe to conclude that a weaker dollar is not the answer for the US external imbalance. And that takes us to the essence of the problem -- America's massive import overhang. Import fluctuations in any economy are, of course, a derivative of the cyclical ups and downs of domestic demand. But there is also an important secular overlay that is traceable to the same structural pressures noted above. On both counts, the United States qualifies as importer extraordinaire. The shift in the global competitive playing field leaves an increasingly hollow US economy with little choice but to rely more and more on foreign production to source internal demand. And the extraordinary burst of domestic consumer demand in recent years -- with personal consumption expenditures holding at a record 71% of GDP since early 2002 -- pushes the internal-demand underpinnings of US imports into an entirely different realm. Little wonder the US continues to lead the global import sweepstakes, with some $1.7 trillion in imports in 2005 --well in excess of dollar-based import bills of the Euro zone (US$1.5 trillion), UK ($0.5 trillion), Japan ($0.5 trillion), and China ($0.7 trillion). In terms of fixing America's external imbalance, for reasons also noted above, I am not optimistic that the answer can be found in the structural, or competitive, angle. Instead, my sense is that the answer lies mainly in the cyclical piece of the equation -- specifically, in the asset-driven excesses of US consumption. With consumption growth running well ahead of labor income growth over the entire four years of the current economic expansion, there can be no mistaking the importance of property-driven wealth effects in closing the gap. Estimates conducted by none other than former Fed Chairman Alan Greenspan put the equity extraction from residential property in excess of $600 billion in 2005 alone -- enough, by his reckoning, to have accounted for all of the decline in household saving since 1995 (see the September 2005 Federal Reserve working paper by Alan Greenspan and James Kennedy, Estimates of Home Mortgage Originations, Repayments, and Debt on One-to-Four-Family Residences). In short, look no further than the asset-dependent consumption binge as a major cyclical culprit behind America's import overhang. This takes us to the most controversial piece of the debate -- the so-called real interest conundrum. In my view, led by the world's major central banks at the short end of the curve, and augmented by the conundrum at the longer end of the curve, the super-liquidity cycle has played the decisive role in taking asset markets to excess over the past decade. First with equities, then bonds, and now property, American consumers, in particular, have come to take excessive rates of asset appreciation as an entitlement. As I see it, the Federal Reserve played a critical role in fostering this outcome -- first by condoning the equity bubble in the late 1990s and then by setting up the now infamous serial-bubble syndrome by slashing its nominal policy rate to the rock-bottom 1% level once the equity bubble burst. The overall level of real interest rates was artificially depressed throughout this period -- sustaining the rise of asset-dependent consumption and a concomitant overhang of excess imports. The Fed, of course, has attempted to normalize real interest rates over the past 18 months, but its 350 basis points of tightening at the short end of the curve has had next to no impact at the long end. Policy-related buying of dollar-denominated assets by Asian central banks has been an important, but by no means exclusive explanation of this conundrum. So has the globalization of disinflation. But for me, the bottom line is clear: If the US wants to come to grips with this imbalance, or if the world wants to address this increasingly worrisome source of instability, the answer can probably be found more in the real interest rate than in the dollar. What Roach leaves out here is what the consequences of raising real interest rates to a sufficient level in an environment of consumer and government overindebtedness: another Great Depression. Whatever the reason, there can be little doubt that the excesses of asset-dependent consumption lie at the heart of America's import problem -- and therefore at the heart of the world's biggest imbalance, the US trade deficit. And, of course, the saving problem is the mirror image of this statement. Lacking in domestic saving -- America's net national saving rate fell into negative territory for the first time in modern history in late 2005 -- the US has turned heavily to foreign saving in order to fill the void. And it has had to run massive current account and trade deficits to attract the foreign capital. Yet there is no free lunch. The imported saving comes at a real cost -- overly-indebted and asset-stretched American consumers, on the one hand, and a collection of US creditors that are under-consuming at home and massively overweight dollars in their rapidly growing stashes of official foreign exchange reserves. I don't buy the idea that these tensions are manifestations of a glorious new era for a dollar-centric world economy. I worry, instead, that as the liquidity cycle turns, asset-driven global imbalances are reaching the breaking point. Yet the optimists have taken to questioning the math behind statistics that they don't want to acknowledge. Here's Brad Setser: Is national income accounting biased against the US?

Feb 05 2006 In a fake news classic, Rob Corddry and Jon Stewart of the Daily Show once pondered how to report "the facts" when "the facts themselves were biased." Michael Mandel seems to think the facts are biased against the US economy. Not really the facts. National income accounting . According to Mandel, national income accounting is biased against the US. It was designed for countries that invest heavily in factories that make things. The US in the 1920s and 1930s and above all the 1940s. Or China today. National income accounting doesn't work for the current knowledge-driven American economy , driven by platform companies that have outsourced all the dirty work of manufacturing. Rather than obsess about all the weaknesses that US shows in the conventional national income accounts - low savings, not-so-wonderful investment, big current account deficits - we should embrace a set of new metrics designed for the Ipod (designed in California, assembled in Asia) economy. Time and other worry warts have it all wrong, in part because it looked at the wrong measures. National income accounting understates both US investment in "knowledge" and brand equity and US "knowledge" exports. To be fair to Michael Mandel, I am exaggerating his argument a bit for effect, and ignoring the caveats in his Business Week cover story. But he clearly thinks the "doom and gloom caucus, trade deficit division" doesn't get the new knowledge economy. Is he right?

Mandel's core argment is that the national accounts understate US investment in the knowledge economy and other intangible assets, understate savings by counting investment as consumption and fails to capture US knowledge exports. I do not have an informed opinion on the question of whether the national accounts definition of investment is dated, and too narrow. Should some of McDonald's advertising budget be considered a long-term investment in McDonald's brand - an investment with a longer half-life than a new PC - rather than just an attempt to sell more burgers today. That would drive up US investment rates. And US savings rates, as both business investment and business savings would rise. Maybe the US invests (and saves) more than the national income accounts show. I don't think, though, that mismeasured advertising investment changes the bottom line: the US now saves a lot less than it used to. The US savings rate may not be negative, but it still fall short of what the US needs to finance all the investment the US does. But that's old thinking according to Mandel. The Gloom and Doom caucus - trade deficit division (I suspect most would consider me a member) misses all the fantastic profits that US firms are making exporting their know-how. It mismeasures the Ipod economy. A country that is the home of the company that owns Eurodisney, Tokyo Disney and Hong Kong Disney and profits from all the Brits lining up to get into Orlando's Disney World must be doing well ... One caveat. Eurodisney is not my example. It belongs to the Harvard economists who conjured up dark matter . I suspect it isn't the best of all examples of US prowess abroad ... According to Mandel, the doom and gloom caucus, trade deficit division, doesn't get the Ipod economy. It also ignores all the gains the US gets from importing human capital. Immigrants educated abroad generate large big windfall gains when they come to the US. India pays for the world class education at Indian Institutes of Technology (IITs), US firms (and therefore US economy) reap the benefits. Mandel: Perhaps the trickiest and most controversial aspect of the shadow economy is how it alters our assessment of international trade. The same intangible investments not counted in GDP, such as business know-how and brand equity, are for the most part left out of foreign trade stats, too. Also largely ignored is the mass influx of trained workers into the U.S. They represent an immense contribution of human capital to the economy that the U.S. gets free of charge, which can substantially balance out the trade deficit of goods and services. "I don't know that the trade deficit really tells you where you are in the global economy," says Gary L. Ellis, chief financial officer of Medtronic Inc., a world leader in medical devices such as implantable defibrillators. "We're exporting a lot of knowledge." I want to touch (hopefully briefly) on both parts of Mandel's arguments. Should a country that is importing human capital also be importing savings from abroad, as Mandel argues? Perhaps. Consider Australia in the 1800s. It imported people and capital from the British Isles. But those resources were invested in the export sector, producing wool, wheat and iron to sell back to Britain. Taking on external debt to build up an export sector (staffed with immigrant labor) is one thing. But that is not what the US seems to be doing. The debt seems to be financing the housing sector. And lots of immigrants seem to be employed in the US service sector. Visit a restaurant kitchen in New York. Or look for domestic help ... Still, I can see why the US might be importing capital from other advanced economies whose labor forces are forecast to fall. Though it isn't immediately obvious why Japan is financing the US rater than say emerging Asia. Or why the emerging world and its rapidly expanding urban labor force is financing the US.

But maybe my concern is misplaced - the US isn't importing savings to build houses and a domestic services sector, but successful, global platform companies that stride the world, sucking up profits from their activities abroad that "old" metrics like the current account don't capture. That too is part of Mandel's argument. US knowledge exports that make Intel's plants in Israel, Costa Rica, Ireland, Singapore and no doubt many other places hum. Pepsi exports knowledge to Ireland, where it now produces Pepsi concentrate for sale back to the US . OK, not that one. It is too obviously tax arbitrage. Coke does it too. I don't buy the broader argument, at least not in full. Mandel didn't mention the Japanese knowledge Toyota exports to its US plants. Or the German knowledge that Mercedes and BMW export to their US (and Eastern European) plants. Or the French knowledge exported in the perfume, fashion and wine businesses ...

The flow of intangibles in the global economy is not one way.

Nor do US firms capture all of the benefits of their "intangible" knowledge exports. A US firm sets up a plant in China, and teaches its employees the secrets of building cars or computer chips. And then a Chinese firm poaches its US firms' employees. This is no doubt good for economic development, as it helps increase the productivity of Chinese firms. But it makes it harder for the US to continue to reap monopoly profits on its knowledge. Or its brands. I also don't think the current account is quite as outdated a concept as Mandel suggests. The current account deficit is not just the trade deficit. It also includes US overseas "income" - as well as the payments the US makes on its external debt. There are obviously enormous issues about the correct measurement of the overseas profits of US firms. But the overseas income of US firms is a big part of the US current account. Indeed, it is the income that the US gets from its firms abroad that has keep the US from making (net) interest and dividend payments on the world. Dark matter and all. Forcing the numbers to reflect your fantasy (creating your reality) is what Enron did. And Ken Lay is still unrepentant, blaming the crash of Enron on a run on the bank'. The parallels are disturbing: Greed, Debt, Incompetence The United States of Enron By ROBERT BRYCE February 15, 2006 Jeff Skilling had a vision for Enron. In February of 2001, he told the company's employees that Enron, would, within five years, be the leading company in the world.

World dominance was the main message that Skilling and Enron's chairman, Ken Lay, imparted to their employees in the video of that 2001 meeting, which was re-played on Wednesday morning in courtroom 9B of the federal courthouse in Houston. Forget talk that Enron was short on cash, or that the mighty juggernaut was overextended and hobbled by competitors. Ignore the doubters, like the journalists at Fortune magazine, who had, a few days earlier, published a story saying that Enron's business model was based on a black box. The company is doing great, Skilling told the Enron employees. We've got a vision for the next century.

It was during the playing of that video that it became clear: the Bush Administration has become Enron. World dominance. The old rules don't apply. Machiavellian vengeance toward naysayers. Corrupt accounting. And holding all of those ingredients together: a heaping helping of hubris, a hubris that leaves no room for doubt or uncertainty. That George W. Bush has morphed into his old pal, Kenny Boy Lay shouldn't be surprising. Enron was, until the 2004 campaign, Bush's biggest career patron. The intrigue lies in the myriad parallels that can be drawn between the Bush regime and the Enron regime. On a personality level, you have the similarities between Bush and Lay: both are the detached executives who couldn't know -- or didn't bother to pay attention to -- what was happening in their operations. Lay, his defense lawyers insist, had no idea that Enron's chief financial officer, Andy Fastow, was cooking the books. Lay was in charge of the big picture. He was the public face of Enron, Mr. Outside. Never mind that Lay was a PhD. in economics who couldn't read a cash flow statement. As for Bush, neither he nor his defense secretary, Donald Rumsfeld, can be held accountable for the torture of Iraqi prisoners that occurred at Abu Ghraib. That was done by rogue soldiers without approval from their commanders. Both Lay and Bush have backed their subordinates, no matter how grievous their wrongdoing. In October of 2001, after Fastow's double-dealing was exposed, Lay insisted that he and the Enron board have the highest faith and confidence in Andy and think he's doing an outstanding job as CFO. In May of 2004, right after the Abu Ghraib scandal broke, Bush insisted that Rumsfeld was doing a superb job and that America owes him a debt of gratitude. The old rules no longer apply. For Enron, it was the old rules of accounting. As Skilling once told Enron's chief accounting officer, Rick Causey, Cash doesn't matter. All that matters is earnings. Enron had blown up the old methods. It was operating in a new paradigm, and those who didn't understand that, well, as Skilling often put it, they just didn't get it. For the Bush Administration the old rules include anachronisms like the Geneva Convention. Bush insist that he's fighting a new, stateless, enemy, and thus the global war on terror cannot be constrained by old treaties, old rules, or the countries that Rumsfeld calls old Europe. That means that illegal enemy combatants can be held at Guantanamo Bay, or in secret prisons in Syria, or elsewhere, for as long as Bush deems necessary. Cheney, plays the role of Skilling. Like the monomaniacal Enron executive who never doubted that his vision for a business that would dominate global markets in everything from natural gas and electricity to paper and steel, Cheney is the true believer in America's global dominance, the one who constantly pushes against old notions that might constrain America's power. If that means torturing prisoners, no problem. As Cheney said shortly after the 9-11 attacks, the U.S. government must, work through, sort of, the dark side. And that means that it is vital for us to use any means at our disposal, basically, to achieve our objective. Opponents of the regime must be dealt with quickly and harshly. For Enron, that meant that stock analysts like Merrill Lynch's John Olson, who never parroted the company's rosy predictions, had to be silenced. Merrill fired Olson after Enron made its displeasure known. For the Bush regime, it meant smearing former ambassador Joe Wilson and his wife, Valerie Plame. Wilson's offense: publicly questioning the story that Iraq was trying to buy radioactive materials from Niger. Opponents who don't follow the script are assholes. That was made clear in September 2000, when Bush, unaware that his microphone was on, pointed to New York Times reporter Adam Clymer and told Cheney, who was standing nearby, that Clymer was a major league asshole. Cheney readily agreed. Skilling used the same term a few months later during an April 2001 conference call with analysts. When Boston hedge fund manager Richard Grubman pressed Skilling on a financial question, Skilling cut him off, and let all of the analysts and his Enron pals know that Grubman, too, was an asshole. Finally, the defense strategies adopted by Bush and his cronies at Enron are exactly the same. That is: everything we did was legal. From the beginning of their trial, the attorneys for Lay and Skilling, Mike Ramsey and Dan Petrocelli, have stuck to that theme. During his opening argument, Petrocelli declared that Enron was no house of cards

It was a wonderful company, a shining star. Ramsey told jurors that Enron didn't fail because of the billions of dollars in accounting shenanigans, it failed because of a market panic. That same tactic has been used consistently by the Bush Administration to defend the CIA's rendition of terror and the indefinite imprisonment of terrorism suspects without charges -- in places like Guantánamo Bay. Last week, about the same time that the first prosecution witness began testifying on the stand in Houston, Attorney General Alberto Gonzales was testifying before the Senate Judiciary Committee, telling the senators that the secret wiretaps that Bush has authorized are legal. And why are they legal? Well, because Gonzales and the president say it's legal. Unlike the execrable Gonzales who has yet to utter a credible word in defense of torture or wiretaps, the Enron attorneys are at least partially correct in their diagnosis of the failure of Enron. It's true that the collapse of Enron was hastened by a market panic. That panic was a direct result of Lay's incompetence. Lay simply did not know how much money Enron had borrowed to fund its global ambitions. Nor did he grasp just how deeply distrusted Enron was by its peer companies. Incompetence. Huge debts. Lack of trust. Just another set of parallels for Kenny Boy and his pal, W.

Robert Bryce is the author of Pipe Dreams: Greed, Ego, and the Death of Enron No matter whom they want to blame it on, the fact is Enron collapsed. Will the U.S. empire and imperial economy collapse as well? Jared Diamond, best known as the author of Guns, Germs and Steel, published another book last year, called Collapse. Diamond defines collapse' as a drastic decrease in human population size and/or political/economic/social complexity, over a considerable area, for an extended time (Jared Diamond, Collapse: How Societies Choose to Fail or Succeed, New York: Viking Press, 2005, p. 3). In Collapse , he argues that societies collapse when bad decisions are made by societies in the face of threats to the basic resources on which the societies are dependent. These bad decisions result from: 1. Failure to Anticipate, 2. Failure to Perceive, 3. Rational Bad Behavior, and 4. Disastrous Values. Rational bad behavior is interesting because it has to do with the character of the society's leaders. After discussing conflicts of interest in societies, Diamond writes: A further conflict of interest involving rational behavior arises when the interests of the decision-making elite in power clash with the interests of the rest of society. Especially if the elite can insulate themselves from the consequences of their actions, they are likely to do things that profit themselves, regardless of whether those actions hurt everybody else.

Throughout recorded history, actions or inactions by self-absorbed kings, chiefs, and politicians have been a regular cause of societal collapses

(p.430-1) Sound familiar? According to Diamond, the challenges faced by today's self-absorbed leaders are these twelve environmental problems: At an accelerating rate, we are destroying natural habitats or else converting them to human-made habitats , such as cities and villages, farmlands and pastures, roads, and golf-courses. The natural habitats whose losses have provoked the most discussion are forests, wetlands, coral reefs, and the ocean bottom. (p. 487) Wild foods, especially fish and to a lesser extent shellfish, contribute a large fraction of the protein consumed by humans . In effect, this is protein that we obtain for free (other than the cost of catching and transporting the fish), and that reduces our needs for animal protein that we have to grow ourselves in the form of domestic livestock. About two billion people, most of them poor, depend on the oceans for protein. If wild fish stocks were managed appropriately, the stock levels could be maintained, and they could be harvested perpetually. Unfortunately, the problem known as the tragedy of the commons has regularly undone efforts to manage fisheries sustainably, and the great majority of valuable fisheries already either have collapsed or are in steep decline

(p. 488) A significant fraction of wild species, populations, and genetic diversity has already been lost, and at present rates a large fraction of what remains will be lost within the next half-century

(p. 488) Soils of farmlands used for growing crops are being carried away by water and wind erosion at rates between 10 and 40 times the rates of soil formation, and between 500 and 10,000 times soil erosion rates on forested land

(p. 489)

The next three problems involve ceilingson energy, freshwater, and photosynthetic capacity. In each case the ceiling is not hard and fixed but soft: we can obtain more of the needed resource, but at increasing costs. The world's major energy sources, especially for industrial societies, are fossil fuels: oil, natural gas, and coal. While there has been much discussion about how many big oil and gas fields remain to be discovered, and while coal reserves are believed to be large, the prevalent view is that known and likely reserves of readily accesible oil and natural gas will last for a few more decades. This view should not be misinterpreted to mean that all of the oil and natural gas within the Earth will have been used up by then. Instead, further reserves will be deeper underground, dirtier, increasingly expensive to extract or process, or will involve higher environmental costs. (p. 490) Most of the world's freshwater in rivers and lakes is already being utilized for irrigation, domestic and industrial water, and in situ uses such as boat transportation corridors, fisheries, and recreation

Throughout the world, freshwater underground aquifers are being depleted at rates faster than they are being naturally replenished. (p. 490) It might at first seem that the supply of sunlight is infinite, so one might reason that the Earth's capacity to grow serious crops and wild plants is also infinite. Within the last 20 years, it has been appreciated that that is not the case, and that's not only because plants grow poorlyin the world's Artic regions and deserts unless one goes to the expense of supplying heat or water. More generally, the amount of solar energy fixed per acre by plant photosynthesis, hence plant growth per acre, depends on temperature and rainfall

The first calculation of this photosynthetic ceiling, carried out in 1986, estimated that humans then already used (e.g., for crops, tree plantations, and golf courses) or diverted or wasted (e.g., light falling on concrete roads and buildings) about half of the Earth's photosynthetic capacity. Given the rate of increase in human population, and especially of population impact

, since 1986, we are projected to be utilizing most of the world's terrestrial photosynthetic capacity by the middle of this century. That is, most energy fixed from sunlight will be used for human purposes, and little will be left over to support the growth of natural plant communities, such as natural forests. (pp. 490-1)

The next three problems involve harmful things that we generate or move around: toxic chemicals, alien species, and atmospheric gases. The chemical industry and many other industries manufacture or release into the air, soil, oceans, lakes and rivers many toxic chemicals, some of them unnatural and synthesized only by humans, others present naturally in tiny concentrations (e.g., mercury) or else synthesized by living things but synthesized and released by humans in quantities much larger than natural ones (e.g, hormones)

(p. 491) The term alien species refers to species that we transfer, intentionally or inadvertently, from a place where they are native to another place where they are not native

. (p. 492) Human activities produce gases that escape into the atmosphere, where they either damage the protective ozone layer

or else act as greenhouse gases that absorb sunlight and thereby lead to global warming. (p. 493) The remaining two problems involve the increase in human population: The world's human population is growing. More people require more food, space, water, energy and other resources

(p. 494) What really counts is not the number of people alone, but their impact on the environment

Our numbers pose problems insofar as we consume resources and generate wastes. The per-capita impact

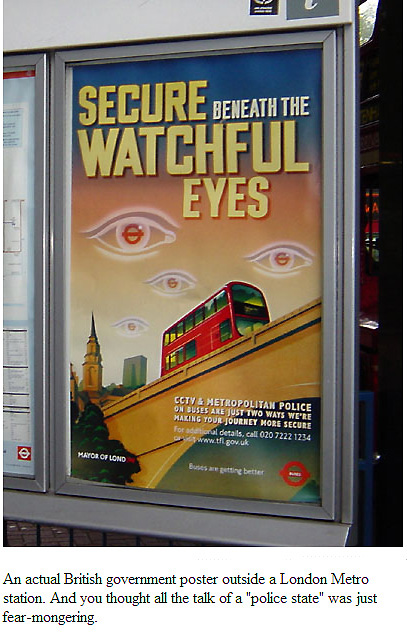

varies greatly around the world, being highest in the First World and lowest in the Third World. On the average, each citizen of the U.S., western Europe, and Japan consumes 32 times more resources such as fossil fuels, and puts out 32 times more wastes, than do inhabitants of the Third World. But low-impact people are becoming high-impact people for two reasons: rises in living standards in Third World countries whose inhabitants see and covet First World lifestyles; and immigration, both legal and illegal, of individual Third World inhabitants to the First World. (pp. 494-5) Now, let's say you are a ruling psychopath, part of the pathocracy, which means you have no conscience whatsoever. But you are smart and you can see these facts. What to you would be the easiest solution? Reduce population! Do it purposefully so that you can direct the reductions to be in your best interests. Why would the pathocracy care to rationally steward resources to provide basics for the most amount of people when wars, genocides, and ethnic-specific weapons can not only solve the population problem but also put (or so they think) themselves on top of the world of survivors?

|

![[Valid Atom 1.0]](/signs/images/valid-atom.png "Validate my Atom 1.0 feed")