It's happening. Much of what we've been predicting for the past year seems to be taking place. The housing bubble has popped, gold and other precious metals are shooting up in price as those with money are rushing to seek shelter.

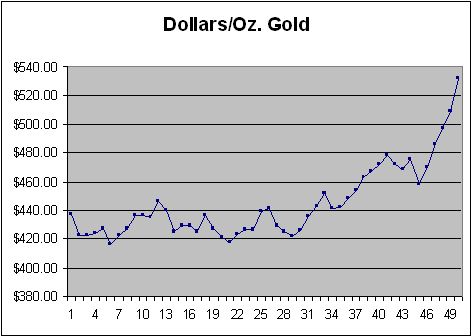

Gold prices seem to have broken through any past barriers. Here is a chart showing changes in the price of gold in number of weeks so far in 2005:

Here is Steven Lagavulin:

A Crisis of ConfidenceAs for the housing bubble:

Gold is on an unbelievable tear lately, blowing right through $500/oz and surging higher every day. And while I don't much talk about day-to-day market news, I think this is an incredibly significant event, and therefore one to take note of. For one thing it means gold has likely broken free of the chains the monetary-control stormtroopers have had it in for more than a decade. Now there's a whole host of reasons why it's in the interest of certain federal authorities to keep gold on a tight rein, but suffice it to say they all boil down to one thing: confidence. Authority is built on a foundation of popular confidence, and the major flagpost of that confidence is monetary strength (ie. strength in the dollar--or at least 'perceived' strength since in the larger scope controlled weakness is actually the integral purpose of the system...).

So it seems appropriate now to paint this picture in the proper light.

In the financial markets there are two ends to every stick as far as price movement is concerned, and such is especially the case with the price of gold. The common-man's viewpoint (which is also the view of the mass media) is simply that the "price" of gold is going up, but this incorrectly implies that the value of the dollar (or any other currency against which it's being measured) is holding stable and that it's only gold itself that is in rising demand. But in the price of any security or commodity, both the thing itself and the underlying currency in question are in flux, as neither one is of stable value. Therefore the price only reflects their value at a particular point relative to each other. This is why it can be observed that in a high inflation environment -- and all things being equal -- the Dow Jones Industrial Average will naturally tend to rise, but that it's a false assumption to believe that it's actually increasing in value. It's simply 'adjusting' itself to the declining value of the dollar.

However our particular case is special in that gold is generally held to be the most stable reference of value we know (when it's not being manipulated), for a host of practical reasons we probably don't need to go into. So the other end of the stick, which is actually the more valid point of view, holds that gold is the reference point by which the value of the dollar is being judged.

So long story short, I think there are a couple of scenarios: either gold has finally broken free of the gold-police and is racing to discover its real value in relation to the dollar and other currencies, or else we're witnessing a decisive plunge in currency confidence -- not just the US dollar but paper currencies in general, since investors are not simply fleeing one currency in favor of another but are effectively fleeing currencies altogether for real asset value (which, by the way, might suggest a possible connection with the recent decline in the real estate market -- the most recent wildly-popular avenue of "real asset value"...).

Of course fans of paper-money (you know, the Gub-mint) could argue that neither case is true, that this is simply an isolated surge in the demand for gold, an investment trend or secular commodity trend or such. But I'd protest that a move of this strength occuring in combination with strong movements in other precious metals, and in further conjunction with widespread social, political and economic crises, that what we're actually seeing is a combination of both these scenarios. In other words, a general crisis of confidence and flight to quality which has overwhelmed the Fed's ability to control the market any longer.

For those who are interested (and who don't regularly follow the deconsumption news room) I'll reference this November Barron's interview with Toqueville Gold Fund manager John Hathaway back in November, where he very effectively makes a case, as I interpret it, that gold is destined to rise simply because investors are fast running out of other options. And that my friends is a crisis of confidence, in a nutshell.

Also I think it's also important to note that in my experience market moves like this almost invariably anticipate a more general awareness in the social sphere....so I would expect to see this important tipping-point echoed in a myriad other ways over the next few months. And I might further add that there are many gold market analysts who have long held that a strong surge in gold would likely place some of those aforementioned monetary-control-freaks in a very disconcerting short-covering situation.

Housing market decline may cost 800,000 jobs, study saysLet's take a closer look at the signs in the crucial Boston market, one of the bubble regions, where asking prices are beginning a free-fall, dropping by a third in many cases:

December 8, 2005

Associated Press

A sustained decline will hit the U.S. housing market next year, costing the nation as many as 800,000 jobs, according to an economic report released Wednesday.

The slowdown is likely to last several years, with as many as 500,000 construction jobs and 300,000 financial sector positions lost, the quarterly Anderson Forecast predicted.

"We expect housing to start slowing the economy this quarter or the next," said Edward Leamer, director of the study done at the University of California, Los Angeles.

...The report cited several signs the decline could be under way:

- New construction of housing in October was down 5.6 percent from the previous month, with new construction of single-family housing accounting for a 3.7 percent dip.

- New-home sales have declined.

- Applications for home mortgages have trended downward since late September as rates increased.

- In some regions, homes are remaining unsold longer and the pace of housing construction is outpacing population growth, which could spell a decline in demand.

"On all these grounds, we believe housing is due for a sustained decline," economist Michael Bazdarich wrote in the forecast. "The remaining questions are how hard the fall will be and when it will begin."

Foreclosures up 35 percent this yearAnother sign that the crash is happening is that asking prices in the Boston area are dropping in many cases by more than $100,000.

By Ken Maguire

Associated Press

December 7, 2005

BOSTON -- Home mortgage foreclosure filings are on the rise in gritty cities and leafy suburbs, according to a new report showing a 35 percent increase statewide through October.

Filings in suburban Reading more than tripled and there's been a 113 percent increase in Lawrence compared with the same period last year, according to Land Court filings tracked by Framingham-based ForeclosuresMass.

"It spans the whole gamut of income levels," said Jeremy Shapiro, president of ForeclosuresMass.

The number of foreclosures filed through Oct. 31 was 9,459, compared with 7,003 in the same 10-month period last year, the report said. Essex County had the largest increase, at 50 percent.

Adjustable-rate and interest-only loans, which are riskier than traditional fixed-rate loans, are partly to blame. They've become popular because they cost less up front, but they require higher payments typically after a year or two.

"A lot of people don't realize what they're getting themselves into," said Jim Wilde, executive director of the Merrimack Valley Housing Partnership, which administers homebuying classes to residents of Lowell, Lawrence and the surrounding towns.

Interest-only loans, in which homeowners don't pay down the principle right away, are "gimmicks in order to qualify (homebuyers) for the first six months or year," Wilde said. "When the principle payments kick in, they're behind the 8-ball."

Wilde said that on Wednesday alone he talked one couple out of signing a "no documentation" loan that would have cost $2,000 a month. The prospective buyers had an annual household income of just $28,000.

"They would have never been able to make the payments," he said.

Among the state's three largest cities, Worcester had the largest increase with 52 percent, while filings were up 42 percent in Boston, and 20 percent in Springfield, Shapiro said.

In the suburbs, Reading had 28 filings compared with just eight in the first 10 months of 2004, the report said. Burlington's filings tripled, from nine to 27. Seekonk had a 163 percent increase, while Wareham was up 103 percent.

Sellers chop asking prices as housing market slowsIn spite of the collapse (I think we no longer need call it an "impending collapse" - it's happening), consumer confidence is rising to allow producers and retailers to extract some more surplus for one last holiday season. A reader wrote in:

Cuts of up to 20% are now common as analysts see signs of a 'hard landing'

By Kimberly Blanton

Boston Globe

December 9, 2005

Boston-area homeowners trying to sell their houses are sharply reducing asking prices -- in some cases, by $100,000 or more -- in response to the sudden slowdown in the real estate market.

Demand for single-family homes has declined as prices have risen in recent years and interest rates have begun to climb, causing the number of properties on the market to pile up.

The median price of a single-family home in Massachusetts has dropped 7 percent in the past two months, to $349,000 for sales that closed in October. But reductions in asking prices of 10 percent or 20 percent are now common in both high and moderately priced neighborhoods, according to real estate agents and listings of homes for sale. In Cambridge, price cuts averaged $300,000 in a sampling of a dozen houses listed in the $1.25 million to $4.3 million price range. In suburbs like Tewksbury and Hopkinton, homes originally listed for around $500,000 have been slashed to the low $400,000s.

"The evidence -- both early data and the anecdotes -- are pointing more toward a hard rather than a soft landing" in the housing market, said Nicholas Perna, an economic consultant in Ridgefield, Conn. "Prices could come down. Could it be 10 to 15 percent? There's no way of knowing, but what we're getting is more clues that you've got a decline in prices underway.

Agents said price cutting began last summer but accelerated in the past two months and is far more frenzied than in 2004, a year of record sales volume.

Today, homeowners in no rush still have the option of letting their listing expire, unsold, and putting the house back on the market in the spring when brokers hope conditions will improve.

But those who need to sell quickly -- couples in the midst of a divorce, employees who are relocating to another region, or owners who are purchasing another home, for example -- may have no choice but to entertain offers they would have scoffed at months or even weeks ago.

"It's unbelievable," said Polly Drinkwater, an agent with Coldwell Banker Cambridge, who has dropped the price on one of her listings $550,000, or 22 percent, since March. These "are very large drops," she said.

Last February, Gary and Susan Kazmer were confident of selling their Foxborough home for $949,900. He had landed a high-level job in Manhattan, and the couple planned to relocate their three daughters during the summer to a house they purchased in Mendham, N.J., with a bridge loan.

They built the Foxborough house on a pond in 1997 and filled it with extras: two marble fireplaces and hardwood floors with dark cherry borders. ''We called it our wow house," he said.

But it attracted little interest at that price, and Gil Campos of Re/Max Real Estate Center in Foxborough lowered the price to $899,000 in early August. Since then, it has been reduced four times, to $800,000. ''That's an unbelievable spiral," he said.

The Kazmers' limbo ended this week, when they accepted an offer, which Campos declined to disclose.

Regarding retail sales and gas prices: [While gasoline prices have fallen, they're still above last year's levels, and home heating costs are also expected to be high.] It'll be interesting to see what happens to gasoline prices about two weeks after the shopping season is over. I've heard it suggested that gas prices fell to accommodate the retail interests and ensure a fairly good Christmas shopping season.That seems to be the case and it seems to have worked, given the fact that economic optimism is on the rise in the United States during the crucial holiday shopping season:

In other words, gas prices fell because one corporate sector (oil) is scratching the back of another corporate sector (retail, Wal Mart) for a couple of key profit months. I wouldn't be the least bit surprised if gas prices went back up to $2.50-2.60 a gallon [after the holidays].

Poll Shows New Optimism About the EconomyHow can people be so optimistic? Is it all tied to oil prices? Are we that easy? Chad Hudson, in Can Consumers Save Christmas? suggests, as does the reader quoted above, that this is no accident:

By JEANNINE AVERSA

AP Economics Writer

People are feeling better about the economy and their own financial situations, a hopeful sign they'll act more like Santas than Grinches while holiday shopping. The RBC CASH Index, based on polling by Ipsos, showed that consumer confidence clocked in at 85.5 in December, the second-highest reading of this year.

The pickup builds upon the rebound in consumer confidence staged in November, when the index jumped to 81. That revival came after confidence had been stuck in the doldrums in September and October, reflecting worries about sky-high energy prices and other fallout from the Gulf Coast hurricanes.

Economists attributed the December improvement to a retreat in gasoline prices, a ramp up in hiring and solid growth being logged by the overall economy.

"I think shoppers will be in a better frame of mind and may be more inclined to spend. It should be a reasonably merry Christmas," said Bill Cheney, chief economist at John Hancock Financial Services. "I imagine shoppers are feeling pretty good about the holiday even if there is some background insecurity driven by heating bills."

The fresh consumer confidence reading came after a string of good economic news.

Last week, the government reported the economy added 215,000 jobs in November, a clear sign businesses got back in the hiring groove after a two-month hurricane-spawned lull.

Another government report last week showed the economy grew at an energetic 4.3 percent rate in the July-to-September quarter despite the hurricanes' ill effects. Many economists are confident solid economic momentum is being maintained in the current October-to-December quarter.

Against this backdrop, the National Retail Federation is predicting holiday sales this year will increase by a solid 6 percent from last year.

Still, just how generous shoppers may be feeling during the holidays will be influenced in part by how much home heating bills pushed up by record high natural gas prices crimp household budgets, analysts said.

Despite the December rise in consumer confidence, it is still lower than it was last December, when consumer confidence stood at 93.9.

...The biggest over-the-month improvement came from a measure looking at consumers' economic expectations over the next six months, including conditions where they live or work and their own financial positions.

That expectations measure rose to 53.9 in December, up from 44.5 in November. This gauge, which faltered dramatically in September and fell into negative territory, has risen since then but is well below the 70.5 reading registered in December 2004.

Consumers' feelings about jobs remained buoyant at 116.5 in December, following a strong reading of 119.8 in November. A year ago, this measure was at 111.1

A gauge looking at consumers' sentiments about current economic conditions rose to 92.8 in December. That was up from 91.1 in November, but was down from 102.7 in December 2004.

Another measure tracking consumers' feelings about making a purchase, saving and other investment decisions increased to 89.5 in December from 82.8 in the prior month. A year ago, this gauge stood at 99.2.

Every time it appears that consumers will start to retrench, some form of stimulus has been injected to spur consumer spending. With the housing boom starting to get long in the tooth, the last boost to consumer spending will diminish. While it is likely consumers will come through for the holiday season, it might prove to be the last hurrah. For retailers, the expansion of retail space over the past several years will exacerbate any slowdown in spending.How many more types of stimuli to consumer spending can there be? Here's Paul Craig Roberts:

An Economy Driven By DebtBut U.S. consumers are not total fools, as consumer credit has begun to fall:

Don't Confuse the Jobs Hype with the Facts

By PAUL CRAIG ROBERTS

Counterpunch.org

December 3/4, 2005

The November payrolls job report was announced Friday with the usual misleading hype. Spinmeisters made the most out of the 215,000 jobs. Looking beyond the glitter at the real facts, this is what we see. 21,000 of those jobs were government jobs supported by taxpayers. There were only 194,000 new jobs in the private sector.

Of those new jobs, 37,000 are in construction and only 11,000 are in manufacturing. The bulk of the new jobs--144,000--are in domestic services.

Wholesale and retail trade account for 20,000. Food services and drinking places (waitresses and bar tenders) account for 38,000. Health care and social assistance account for 27,000. Professional and business services account for 29,000. Financial activities gained 13,000 jobs. Transportation and warehousing gained 8,000 jobs.

Very few of these jobs result in tradable services that can be exported or help to close the growing gap in the US balance of trade.

The 11,000 new factory jobs and the 15,000 of the previous month are a relief from the usual loss. However, these gains are more than offset by the job cuts recently announced by General Motors and Ford.

Despite the gain in jobs, total hours worked declined as the average workweek fell to 33.7 hours. The decline in the labor force participation rate, a consequence of the shrinkage in well-paying jobs, masks a higher rate of unemployment than the reported 5 percent. The ratio of employment to population fell again in November.

Average hourly earnings (up 3.2 percent over the last year) are not keeping up with the consumer price index (up 4.3 percent).

Consequently, real incomes are falling.

This is not the picture of a healthy economy in which growth in high productivity, high value-added jobs fuel the growth in consumer demand and provide savings to finance Washington's red ink. What we are looking at is an economy that is coming unglued from the loss of jobs that provide ladders of upward mobility and from massive trade and budget deficits that are resulting in unsustainable growth in indebtedness to foreigners.

...Populations are hard pressed when the prices of goods rise relative to the price of labor, because this makes it impossible for the population to maintain its standard of living.

The US economy has been kept alive by low interest rates, which fueled a real estate boom. Consumers have kept growth alive by refinancing their home mortgages and spending the equity in their houses. Their indebtedness has risen.

Debt-fueled growth is qualitatively different from economic growth that results from an increase in high value-added jobs. Economists who look at the 3+ percent economic growth rate and conclude that things are fine are fooling themselves and the public. When the real estate boom ends, what will be the source of new spending power?

Consumer credit slides in OctoberAny time recently that consumers have gotten too confident, they start scaring us about Bird Flu. Then, when people get too scared to spend, they start circulating positive economic stories. It looks like we are about to shift from positive stories to scare stories about Bird Flu:

Reuters

Wednesday December 7

WASHINGTON - U.S. consumer credit unexpectedly slid by a record $7.20 billion in October, on a big drop in loans taken for cars and boats, a Federal Reserve report showed on Wednesday.

The central bank said total consumer debt outstanding fell 4 percent to a seasonally adjusted $2.157 trillion from a revised $2.164 trillion in September. The rate of decline was the steepest since December 1990, and the dollar drop was the largest fall on record, the Fed told reporters.

Wall Street analysts polled by Reuters had expected a rise of $5.0 billion in consumer credit in October.

The Fed said non-revolving credit -- made up of closed-end loans for cars, boats, education expenses and holidays -- fell $5.58 billion in October.

Revolving credit, which includes credit and charge cards, dipped $1.63 billion.

Reports detail bird flu effects on USWhat the heck is that last statement all about? "Enjoy themselves?" I guess we can expect to see some agents provocateur providing the excuse for a crackdown during an epidemic.

By Maggie Fox

A pandemic of bird flu could cause a serious recession of the U.S. economy, with immediate costs of between $500 billion and $675 billion, according to two estimates released on Thursday.

Both assume the H5N1 avian influenza now destroying flocks of poultry across Asia and parts of Europe makes the jump into humans and causes serious disease.

So far, H5N1 has killed 69 people and infected 135, but world health experts say it is very close to mutating into a form that easily passes among people.

If it does, it would likely closely resemble the 1918 pandemic strain of flu that killed anywhere between 20 million and 100 million people during World War I, both reports say. This means 30 percent of the population would be infected and more than 2 percent would die, the report from the Congressional Budget Office presumes.

"Further, CBO assumed that those who survived would miss three weeks of work, either because they were sick, because they feared the risk of infection at work, or because they needed to care of family or friends," the report reads.

"In addition to workers' absences, many businesses (such as restaurants and movie theaters) would probably suffer a falloff in demand because people would be afraid to patronize them or because the authorities would close them."

Doctor's offices and hospitals would be overcrowded, the CBO predicts.

"Currently, the United States has approximately 970,000 staffed hospital beds and 100,000 ventilators, with three-quarters of them in use on any given day. As a result, shortages could occur in critical areas such as ventilators, critical care beds, and drugs to treat secondary infections," the report reads.

HOSPITALS SPREADING INFECTION

NHospitals would have difficulty controlling infection and might become sources for spreading the illness, the CBO said -- a fear echoed by another group, the National Center for Policy Analysis.

A second report from New Jersey based WBB Securities LLC estimated 35 percent of the population would become ill and 5 percent would die.

It predicts a one-year economic loss of $488 billion and a permanent economic loss of $1.4 trillion to the U.S. economy.

"If the influenza affected humans at the same level of virulence as the current H5N1 strain, practically all patients would require hospitalization, which would result in a shortage of some 6.5 million hospital beds per day during the pandemic," the WBB report reads.

"Police, fire, sanitation and other critical service providers will be strained with short staff and overtime work, which will impact municipal and state budgets," it adds.

"There may even be civil disturbances caused by people who either believe they can take advantage of the situation or who feel they have little chance of survival so they may as well enjoy themselves while they can."

Finally, in honor of the 25th anniversary of John Lennon's assassination, here is a song he wrote about economics, class power and the Pathocracy. (See also the amazing interview of John Lennnon by Tariq Ali and Robin Blackburn in Counterpunch last week).

Working Class Hero

by John Lennon

As soon as your born they make you feel small,

By giving you no time instead of it all,

Till the pain is so big you feel nothing at all.

A Working Class Hero is something to be,

A Working Class Hero is something to be.

They hurt you at home and they hit you at school,

They hate you if you're clever and despise a fool,

Till you're so f------ crazy you can't follow their rules.

A Working Class Hero is something to be,

A Working Class Hero is something to be.

When they've tortured and scared you for twenty odd years,

Then they expect you to pick a career,

When you can't really function you're so full of fear.

A Working Class Hero is something to be,

A Working Class Hero is something to be.

Keep you doped with religion, sex and T.V.,

And you think you're so clever and classless and free,

But you're still f------ peasants as far as I can see.

A Working Class Hero is something to be,

A Working Class Hero is something to be.

There's room at the top I'm telling you still,

But first you must learn how to smile as you kill,

If you want to be like the folks on the hill.

A Working Class Hero is something to be,

Yes,

A Working Class Hero is something to be.

If you want to be a hero well just follow me.

If you want to be a hero well just follow me.

© Northern Songs Ltd

Reader Comments

to our Newsletter